Imagine a black box.

Your job is to earn and save as much money as you can. You put the cash saved into the black box…into your compounding machine.

Once you put the cash inside the box and close the lid, the magic starts to happen.

Inside the black box the most powerful force in the universe gets to work and your money starts to grow prodigiously. You start with a few thousand pounds and end up with hundreds of thousands, maybe millions.

If you are a bit lazy (and who isn’t?) and yet still want to get rich (and who doesn’t?) then this is The Path for you. We want our money to do as much of the work as possible for us. Yes, we are going to have to save hard…but the earlier we get started, the more of the heavy lifting that compound interest can do for us.

What powers the machine?

The results generated by your Compounding Machine will be driven by:

- The % of your after tax income you put into the box

- How quickly you get the Compounding Machine started

- What asset allocation (i.e. the mix of assets) your Compounding Machine runs on

- The fees that are taken out of your box

- Which fund(s) you choose

All of these elements are important but please note the order I have put them in.

The savings rate is vital. At a 50% savings rate, you will go from broke to financially independent in about 18/19 years. But, at the start of your journey, the most important thing is just to save something (anything) every month. The point is to get into the habit regardless of the amount. Pay yourself first and invest on auto-pilot.

When should you start? Well, the best time to plant a tree was 20 years ago, the second best time is now.

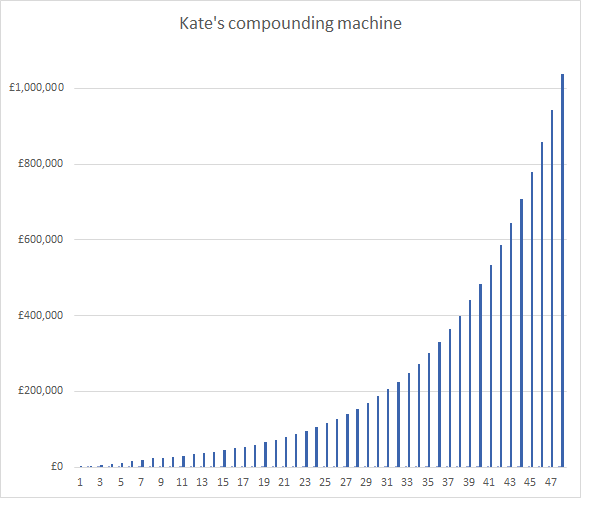

Kate’s compounding machine

To illustrate the power of starting early, let’s return to the example of Kate…a bright school leaver who gets a job aged 18. Kate does not go to university to learn how to eat vodka jelly but instead gets a job, avoids student debt and is able to start saving after 6 months.

Over the next 7 years, our heroine does well and learns stuff at work that actually helps her in life. Things like how to work hard, deal with people and use basic arithmetic. And she does not spend all her salary on shit stuff. Instead she saves, paying herself first every month, setting up a direct debit to stash £167 per month for a total of £15,000 over that period.

Kate directs her monthly savings into a low cost equity index tracker, saving £2,000 per year until age 25 when she stops making contributions into her pension and never saves another penny. Kate does nothing with her pension for the next 40 years and, as a result, Kate gets the same annual return (~10%) as the S&P 500 has done over the last 100 years or so.

At age 65, Kate fires up her laptop and is pleasantly surprised to see that her £15,000 of contributions have grown to just over £1 million. True, inflation means that a million pounds isn’t worth as much as it used to be. But still…not too shabby. You can check out the maths for yourself here.

What does that look like?…BEHOLD THE MIGHTY J CURVE OF COMPOUNDING:

Market predictions are a waste of time

It is traditional at this point for some clown someone to start questioning whether 10% annual returns are realistic in future. We won’t be playing that game here. No one has a crystal ball and no one knows what future returns will be.

The bear case sounds smarter, perhaps because in most areas of life smart and sceptical people often do better. But there are no IQ prizes in investing. A 10% a year return from a stockmarket tracker fund achieved by a person with average intelligence beats a 2% return from a complex multi-asset approach achieved by someone who went to Harvard (someone should really tell hedge fund investors that).

When it comes to predicting future returns, there are 2 types of people: 1) those that don’t know and 2) those that don’t know they don’t know.

What we do know is that, using The Rule of 72, the money inside your compounding machine will double every 9 years at an 8% annual rate of return. At a 10% rate of return the money will double every 7 years. The higher the returns, the quicker your money doubles in value.

Fuelling the machine

We need to choose the fuel for our compounding machine. Just saving into a bank account is like trying to power a full size car on itty-bitty AAA batteries…you wont get very far or very fast. The same applies to bonds: they can’t power your engine, they can only act as a store of value and a shock absorber.

To power your compounding machine properly, you invest in wealth-creating assets and that means the stockmarket or property (and maybe some venture capital & crypto for the brave).

Of these, the stockmarket is easiest (and arguably the safest) to invest in. When you own a global tracker fund, own a slice of the biggest companies in the world and reap the rewards of progress. As time goes by you win as human beings get better at making stuff, using technology and solving problems.

Once you have paid off expensive debt, the best thing to put in your compounding machine is a low cost global tracker fund (such as VWRL or VRXXB in the UK).

Patience

The J curve illustrates the huge and exciting opportunity…and also the problem.

The problem is that the first 6 or 7 years are B – O – R – I – N – G. If you are looking to investing for your excitement in life, you’re looking in the wrong place. By all means take up para-gliding, running with the Bulls at Pamplona or chainsaw juggling…just don’t expect to get that buzz from your compounding machine in the early years.

Better to think like a gardener. Once you have planted your seeds, there’s no point digging them up and looking at them every week to see how they are getting on. Be patient: the time always passes and the future always arrives.

Once you have your compounding machine set up correctly, the less tinkering, the better. I love those studies done by online stockbrokers where they analyse the results achieved by their clients and found that the ones that did the best were those that had died (and the category that did second best had forgotten their log in details).

It may sound like a small point but one of the things I like about Vanguards ETFs (e.g. VWRL) is that dividends are paid every quarter and that’s a regular morale boost and reminder that your compounding machine is working.

If you are naturally impatient, that’s fine…just channel your impatience into your career. Take a qualification, win clients, beat your targets, learn to sell. Make yourself more valuable!

Everything compounds…its not just your stash. If you are doing it right, your salary, your knowledge and your ability to solve problems should grow exponentially as you go through life. The more capital you have (not just money but social capital, reputation, ability to reach an audience) the more effective you become.

Do you really understand compound interest?

It’s important to understand the J curve both objectively and emotionally.

Objectively, the maths is the maths. There’s no point arguing with it…that’s like arguing with gravity.

But you also need to understand it emotionally. Here’s the million dollar (or pound) problem. We are monkeys programmed to operate in the here and now. Our untrained brains are well-adapted by evolution to solve the problem of what’s for supper tonight. But they are absolutely shite at focusing on saving for the long term.

So you have to use your rational mind (the weakest part of the brain) to overcome your chimp brain. This is a bit of a David vs Goliath fight…but its a fight that your inner David can win by carefully targeting his effort.

Here’s a powerful way to tell if you understand compound interest or not. Are you ready? People that understand compound interest, earn it. People that don’t, pay it.

Why you must get out of debt

Imagine that we could invest the money in our compounding machine and get annual returns of 23% per year. That means £10,000 turns into £20,000 in just over 3 years.

Impossible you say? Well, my credit card provider recently wrote to me informing me that the interest rate on any balances not paid off every month is 23%. So millions of credit card holders with debt balances have a guaranteed way to earn 23% a year.

If you are reading this and have any credit card debt, that shit needs to get paid off before anything else. If you have credit card debt, you do not go on dates, visit pubs, restaurants, shops, bookmakers, strip clubs, sports fixtures nor attend property investment or timeshare seminars. In the immortal words of Fergie: take your broke ass home. YOU GO TO WORK, THEN SLEEP, THEN REPEAT UNTIL THE DEBT IS GONE.

Being in debt is like your compounding machine being in reverse gear. Imagine you are in a rusty pick-up truck in the Arizona desert with no aircon, stuck in reverse gear with the radio playing Country & Western music as you accelerate backwards towards the edge of the Grand Canyon. That’s how bad having credit card debt is.

Why doesn’t everyone get taught this at school?

Given how important compound interest is, it’s baffling to me how few people understand it. And how few financial “experts” teach it properly.

If schools taught useful information for life (rather than conformity) they would teach the power (and the maths) of compound interest.

If all personal finance journalists / writers were genuinely interested in spreading financial literacy, they would major on this stuff rather than coupon advertising, product marketing and affiliate links.

No one else is coming to save you. If you are reading this and haven’t got your compounding machine set up yet, it’s time to take action.

Barney

New articles appear first on my Substack : https://theescapeartist1.substack.com/

If you’d like to discuss career coaching or financial coaching, please set up an introductory call with me here.

Amen brother! I’m almost out

nice article, thank you and enjoyed listening to you on MoneyBox. I have less than 5 years to go!

Amen, Amen and Amen!

nice post and it chimes with something I was thinking of recently too.

The temptation for many (myself especially) is to think more about how the box works and like a tuppeny-pusher – when’s the right time to put money into it.

Also, which box to put money into and then should we start switching the boxes around like a magician?

The truth is that when I look at my performance vs. the market – all my meddling has not really been worth it (£/hour meddled) and I would have been better finding a low cost ETF tracker from day one.

Patience is the big barrier I see with people my age; they just don’t want to see the long-term. I suppose that’s understandable given the uncertainties young people are facing in the present with the seemingly impossible task of buying a home, but the amount of apathy concerns me for when they reach their twilight years.

Great hearing you on Money Box even if the presenters liked to speak over everyone 🙂

Yes, patience is something most people don’t have enough of!

You might need a footnote for pedants. Strictly speaking, compounding happens when interest earns interest, or dividend income buys new shares. Starting with £X and ending with £Y doesn’t necessarily involve compounding – although using a PRETEND compound annual growth rate (CAGR) to work out a return is a useful mathematical tool.

As a student I am doing this at a much lower scale than those in work (I assume), but I hit the 5-figure milestone after 3 years! onwards and upwards?

I am invested into the Vanguard FTSE Global All Cap Acc fund, I feel like this is a good fund but I don’t see it recommended regularly, should I switch to one of the funds you recommend or just leave it?

Hi all,

Should we do something about financial education for teenagers and young adults? First step would be to understand what is being done right now. I vaguely recall that in the UK something on personal finance has now gone into the curriculum (I could have this wrong) and certain civil society organisations are working on this. Has anyone got that insight/ done the research?

I’m based in the Netherlands, but am British. I work in both countries (and will continue to do so beyond FI). I’m now in my 30s, but distinctly remember talking to a friend at university when I was 19 baffled by credit cards wondering why I was not taught about money at school. Took me until 28 to have the full financial panic attack and turn to FI blogs to work it through.

Curious if anyone else would be interested in working on this together / is already working on this and would be interested in my support.

Kat

Kat – My personal opinion is that you can’t save everybody and whilst the likes of http://www.retirementinvestingtoday.com have made it their mission to save the masses, so too are the folks at MoneySavingsExpert.

Ultimately, the idea of FI is a bit like Dieting. We all want beach bods (or wallets) but few will ever look as good as the photogenic folks who will tell you about just how frugal they are (whilst doing alright from their ebook and ad-revenue).

Personal responsibility is the only choice in my mind – put on your own lifejacket before saving others.

Found your blog a week ago and have probably read most of it by now (thanks flu!)

I am 28 and bought a house this year, and am at a net worth of about £30k.

I have a small car on finance after the cheap(ish) banger I bought cost me £3k in repairs in a year and cut out as I tried to cross a busy junction. After that I decided that a 7 year warranty and a monthly payment was worth it for my peace of mind.

I don’t have a big city job and left London a few years ago, and actually cut my hours down for my mental health recently; but your content is helping me to see that I actually could get to Financial Independence – or at least be much better off; without the need to get a crazy high paid job again.

Anyway, just wanted to say thank you for all of this great content!!

[…] How to construct a compounding machine – The Escape Artist […]

Hi EA. First, let me say that I am a convert. However, the path to financial liberation is never as smooth as your example suggests … unfortunately there are evil forces at work such as inflation, and whilst for purposes of illustration we can assume a steady rate of inflation, or more usually, a net rate of return after inflation, the reality is that inflation and rate of return rarely track smoothly together. Why am I being a party-pooper – I guess that’s down to my chimp mind, especially if I expect to see a steady progression in wealth accumulation, and it isn’t so. I find my best strategy is to make regular contributions, and leave it to belief in the “investment fairy” to provide, rather than suffering from doubt from a thousand cuts – if you’ve read Taleb Nassim’s Fooled by Randomness you’ll understand where I’m coming from.

Just as an aside, I can never make-out why people ascribe such significant to Einstein’s famous quote on the ‘wonders of compound interest’ – he was, after all, a physicist, not a financial expert, nor, perhaps even more pertinent given what we understand about poor financial decision-making, a psychologist. For my money, Kahneman and Tversky have done much more for improving the everyday man-in-the-streets chances of achieving FIRE than anyone else … I have meet the enemy and the enemy is us!

Good article. I disagree with your views on anything non-equity, however. There is a place for most types of assets in most peoples’ portfolios.

And better than a 23%IRR here is a guaranteed 400% annual return: https://www.youtube.com/watch?v=2U_dfKGbLpY

Interesting comic video – I haven’t been able to find a 10.5l bottle of whisky but maybe I’m not trying hard enough

One added bonus for Scotch drinkers is that after 6 months of nothing but Black Grouse, you’ll maybe never touch a drop of the stuff for the rest of your life.

IRR = Infinity!

Compounding is hard because the feedback mechanism is so long. But if done correctly, it leads to massive returns, i.e. Warren Buffet’s wealth.

[…] HOW TO BUILD A COMPOUNDING MACHINE […]