This post is a <thought experiment> in risk taking for the young and the brave. It is most definitely <not> advice that applies to everyone.

Let us start with the brutal truth…buying a house is sliding beyond the reach of more and more people.

To get on the housing ladder in your 20s or 30s now takes a top job, inheritance or extreme measures.

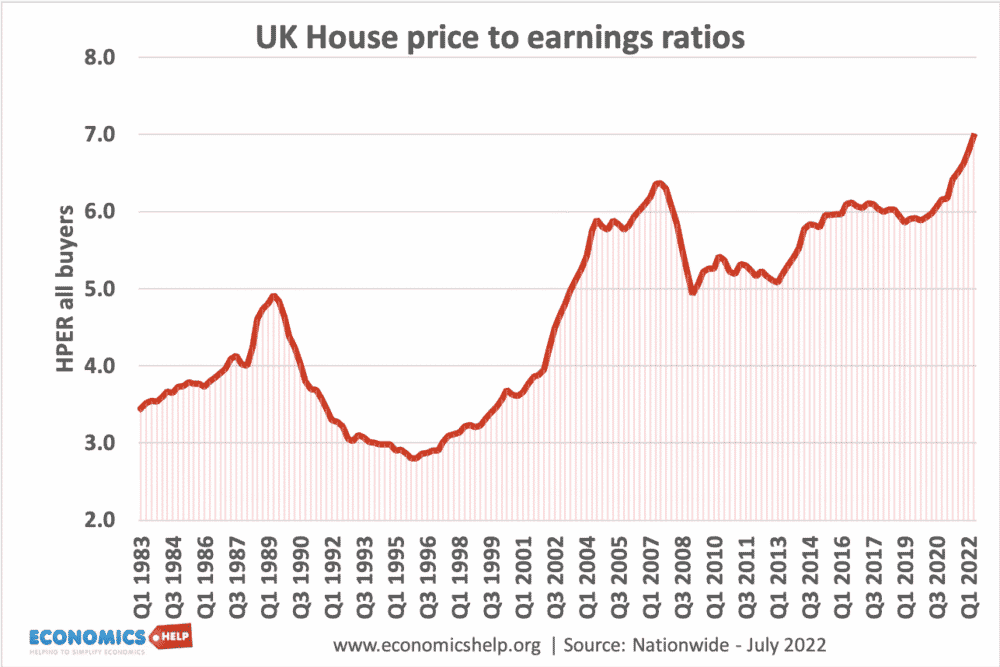

In 1970, you might have been able to buy a house for approximately 2x the annual average income.

Now the price : earnings ratio for UK houses sits over 7x average income.

By this measure we got a LOT poorer…and just skipping the smashed avocado on sourdough toast is not gonna be enough to fix that.

More government intervention is not the answer to this problem, because Government is the main <cause> of the problem.

If The Starmer Regime wanted to help ordinary people buy a house, it would:

1) Print less new money (and let asset prices deflate);

2) Restore border controls & reduce net inwards migration;

3) Speed up planning permission by reducing bureaucracy

I don’t know about you but I won’t be holding my breath on this.

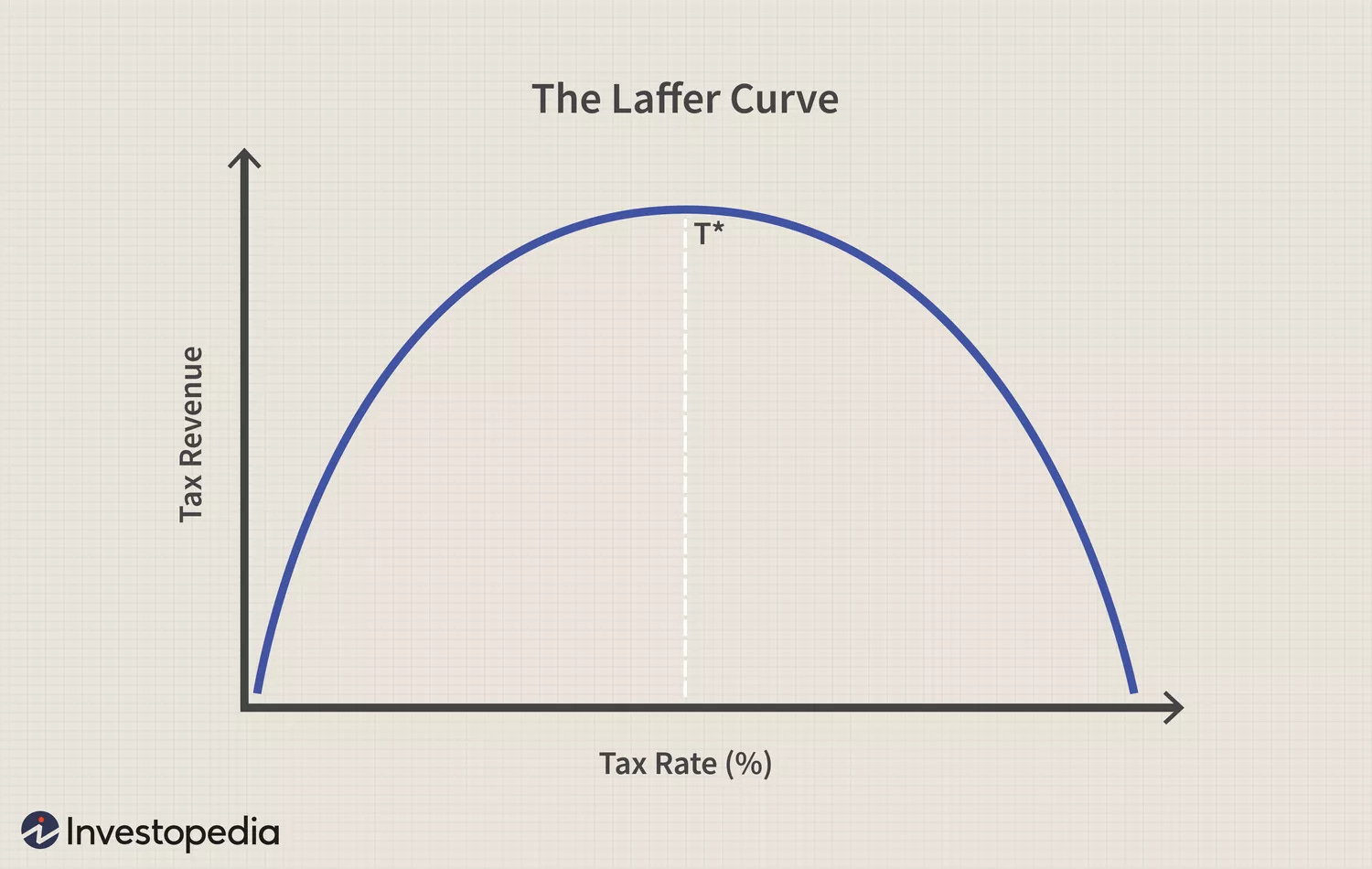

They won’t stop printing money because the government is addicted to overspending and pointless interventions. The UK tax base is screwed: income tax is already at the top of the Laffer Curve.

Beyond this point, higher % rates just increase avoidance and reduce tax revenues.

You can either have open borders OR you can have a welfare state. But you can’t have both. You have to choose. A government’s duty is (or should be) to choose the interests of its own citizens first.

They won’t reduce bureaucracy because that is the one thing that this government seems to believe in above everything. The Starmer Regime is government by public sector bureaucrats FOR public sector bureaucrats.

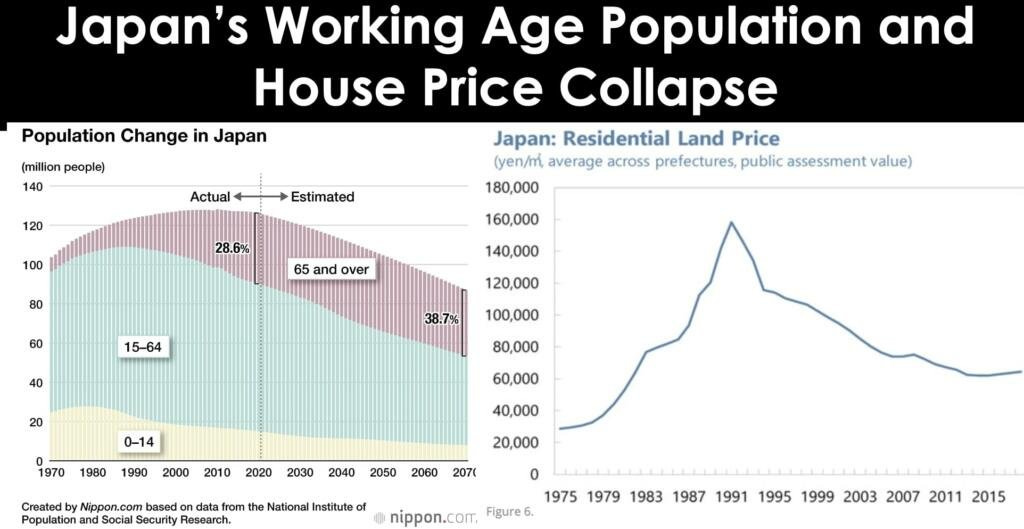

As a brief side-bar, Japan shows that there is another way.

If we want to see what would / could have happened to house prices in the UK with lower net inward migration, Japan gives an illustration.

There are now many empty houses in Japan and, unsurprisingly, Japanese house prices have fallen compared to the UK, Australia, Canada and USA.

There are no guarantees in life.

We are going to have to take some risks…hopefully intelligent risks where the upside > downside.

What will give us our best shot at the prize?

1) Ignore all boomer financial advice about cash ISAs, bonds, 60:40 portfolios, pensions etc

I am sorry but most of the traditional advice for the old / affluent / sensible simply does not apply to those setting out in the world today.

There is a sense in which FIRE blogs were the last gasp of The Post-War Boomer-Retirement Complex.

Frugality is NOT enough. You can’t just penny pinch your way to buying a house in the UK…let alone to financial independence.

You are going to need to earn good money. You are also going to need to throw away (or at least update) much of the old investing advice. LifeStrategy 60:40 etc etc is NOT good enough. Bonds are guaranteed to lose value over the long term. STFU about the interest rate on cash ISAs etc – it’s all irrelevant.

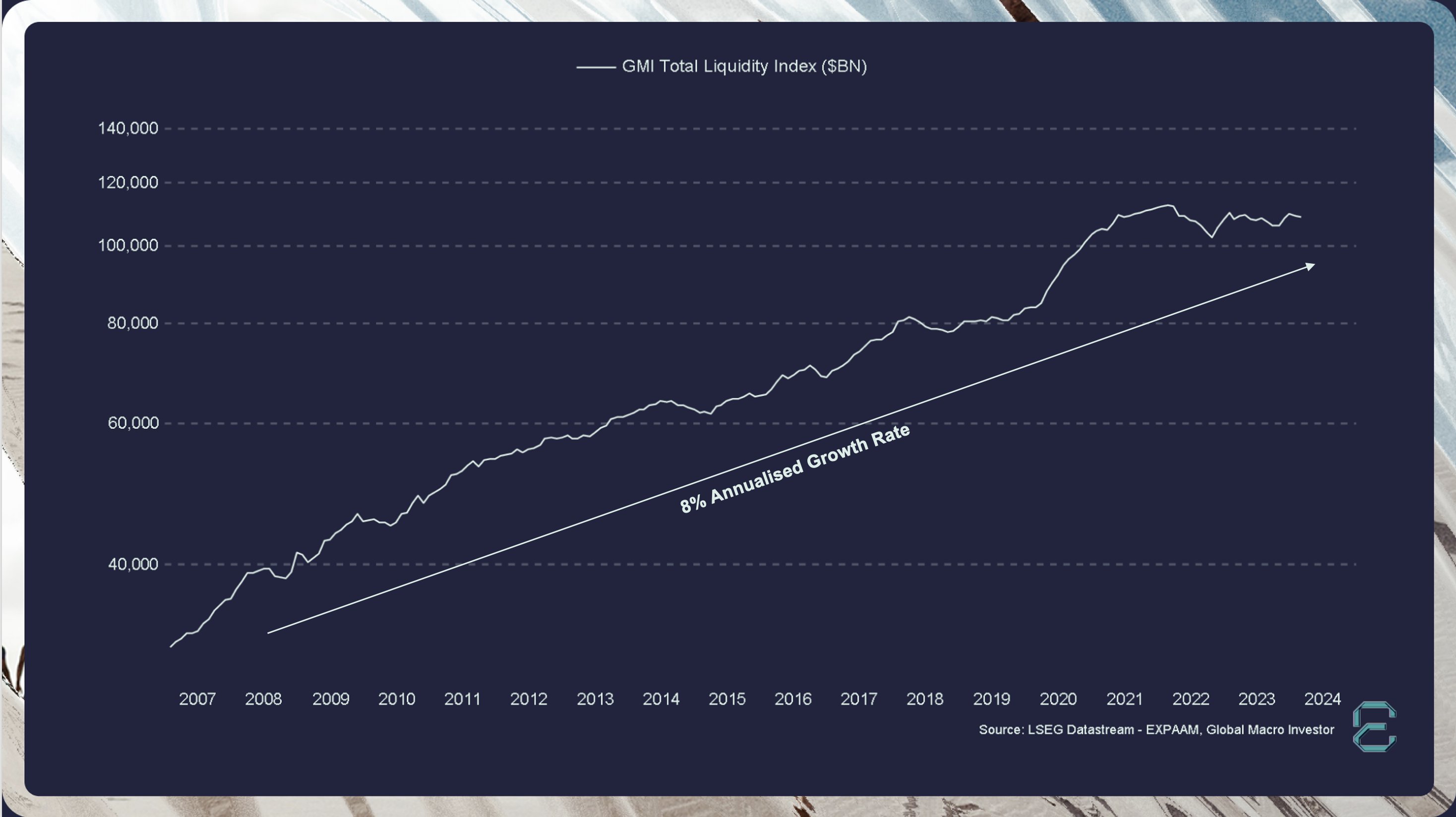

As Raoul Pal explains, UK and other Western governments print new money at something like ~8% per year (it varies but let’s say 8% on average over the cycle). They do this to service their excess spending & debts. That 8% is the rate at which your cash or fixed income holdings are being devalued each year.

The 8% per year debasement of currency is also the tailwind behind rising asset prices…most notably houses.

So…all this means that if you are saving & investing to buy a house, you need to take more financial risk.

If you currently have basically zero net worth and no chance of getting on the housing ladder WTF have you got to lose??

I would go a step further: if a youngster currently has net worth less than say £25,000 and no real chance of getting on the housing ladder WTF have they got to lose??

2) Get a job

When it comes to college, you either go big or go home. The middle ground is a trap.

Ignore college + debt unless you do law, medicine or STEM degree at a Russell Group University. Computer Science at Cambridge? Fine.

Victimhood Studies at Shitbag College, not so much.

Not only is university not the golden ticket anymore, much of it is now actively harmful. There’s the debt of course. But it’s worse than that.

University acts as one of the main supply chains for identity politics. All the crazy woke / trans / intersectionality stuff is rat poison for mental health.

3) Do something hard

You have to have something that makes you more valuable and provides a path to autonomy and financial freedom.

This means doing something HARD…something with potential for career capital and scope for your own business (e.g. apprentice electrician or plumber or beautician or IT consulting services).

Last week I witnessed a joyous triumph in my career coaching. I had been coaching and helping the job search of a young guy (aged 27) who was stuck in a dead-end minimum wage job as a van driver. Not a comfortable place to be when self-driving cars, AI and The Robots are banging on the van door.

He has just been offered a job as a trainee electrician. This provides A PATH for progression to self-determination and self-employment. Maybe a path to employing others and focussing on the marketing, pitching and quality control. It provides a path that will make him robot-proof.

I have lots of clients who earn big money working in Big Tech or Big Law or in Finance. But there is something great about being able to help someone “normal”.

4) Live at home for free

Living with Mum & Dad is one option. Ideal for hard core stashing.

Alternatively flat sharing…the more the merrier. Do not isolate yourself from the world. You probably don’t have clinical ADHD (sorry) or any depression or anxiety that a 10 mile run wouldn’t cure.

When you are young, lodgers can be a quality of life upgrade not just a way to save money.

5) Pay yourself first

You do NOT save “what’s left at the end of the month”. You save as much as you can at <the start> of the month.

You live a low cost lifestyle with minimum waste, no bling.

You could say that minimalism is necessary but not sufficient.

I prefer minimalism to frugality. The problem with frugality is that it usually comes from a place of fear, a scarcity mindset.

6) Asset allocation

Technology has been in a secular bull market since 1990. We don’t care about cyclical volatility…we accept that as the price of admission.

We are looking for assets that offer the best risk-adjusted returns…and that means tech / crypto.

Version 1) 100% crypto

Version 2) 50% Nasdaq tracker, 50% crypto

but top 3 tokens only…NO MEMECOINS & NO SHITCOINS.

7) Monthly Dollar Cost Averaging (DCA)

No trading, no market timing.

Pay yourself first and as soon as you have been paid, Dollar Cost Average EVERY MONTH into your asset allocation of choice.

8) Rinse & repeat for 4 years

(ignoring FUD…Fear, Uncertainty & Doubt during crypto winters…perhaps during 2026 and 2030 if Raoul Pal is correct?)

9) Take chips off the table during The Blow Off tops

The blow off tops are the time when you scale out and take profits. No one knows when exactly this might be but you could tell in August 2021 that we were in a speculative phase (I called this top at the time on The Escape Manual).

10) Buy a flat / starter home for cash

This path is not easy. Yes, it’s risky but that depends on your situation and how much you have to lose.

Like I said, there are no guarantees in life…and there will be volatility. Lots of volatility.

But this at least gives someone a fighting chance to buy a house in their 20s (and eventually to achieve financial freedom).

Love to everyone

Barney

New articles appear first on my Substack : https://theescapeartist1.substack.com/

If you’d like to discuss financial coaching, please set up an introductory call with me here.

Just read this the other day, oddly enough I recently noticed that I’m able to purchase a house and I’m a couple months away from my 30th birthday. But then I’m not talking about the “Average Dutch House” some media outlets present, which according to them cost €500.000 nowadays. I’m talking about a house about 60-80 m2, €270k-€300k price range for a single person. At the moment, I’m not planning to buy a house, I moved out of my parents house to a “Free Sector” rental apartment (as there is a separation between Social Housing in the Netherlands – max €900 rental price monthly, not allowed to earn more than €50k yearly – and Free Sector rental where prices also are limited nowadays). Complaints from people my age are quite numerous and we have too little houses available etc. etc.

So, #1, what did I do? I happened to stumble upon FIRE during my years as Polytechnic (HBO) university student, but I was already introduced to investing when I followed an Bookkeeping vocational course (MBO). Maybe I had a head start on my peers regarding financial knowledge, which probably became larger because I read a lot about investing and followed the FIRE blogs. When I started working, I already had a net worth of about €12k, which was the cash I saved from my internships (I had about 5 before finishing my studies) and the side job in a warehouse on Saturdays. Mind you, it might look like smooth sailing, but I was very anxious about whether I could hold get a job in the first place, and then be able to hold this job. And the second caveat is that my parents don’t have much cash to give, as they’re Cold War migrants from Eastern Europe and didn’t have much dimes to spare. I’m not expecting any windfalls in my life, I had to save everything myself. Moving on, I managed to find myself a job at a machine factory, and a pay which was above average. And then I got some pay raises, I managed to impress some higher ups I guess. I lived at home for about 3 more years after getting the job, then the house I live in now happened to come free. About #4, I can now appreciate that I do not live with Syrian refugees with a desert day-night rhythm below me, a mental nutjob neighbour to the right and a neighbourhood which has been taken over by migrant kids. Nowadays with the investments and savings I made in the Vanguard funds, I have a net worth of about €70k.

#2, My decision for now is not to buy a house. One is that I’m not happy with my job as is now, lack of direction, we got taken over 1,5 years ago and things shifted since then. Besides this, also the lack of opportunities at my current job, boredom, lack of ambition within the workplace (and I want to improve things and learn/grow), makes me feel stifled. I think this is my main unhappiness point at the moment. Two, if I were to find a girlfriend in the next years, then I probably need to move once again when the house becomes too small. Means double costs for the bureaucratic hurdles in the process (tax-deductible, but still could be like €10k-€20k, didn’t run the numbers) and double costs for styling of the house. Third, I don’t want to be bound to my current region, I like the mental freedom it gives. Fourth, I don’t believe the prices can’t go much that much higher, if the AI bubble is real then the mortgage could get “underwater” (even though I know that in the past housing prices went back up again, but how long will it take?). Fifth, the housing market is complete bollocks, sometimes you don’t even have a full day to decide whether you want said house. There are currently serious environmental risks bound to Dutch houses (like slightly sinking homes in some areas). Sixth, in regards to taxes, housing vs investing doesn’t really make a difference when I last calculated it. But with housing you do have the hidden costs etc.

So there you have it, I’m not entirely fulfilled with my current situation, but as an old colleague of mine once said: “It’s better to be unhappy with money than happy without money”. And in relation to the house of my parents, I live in relative mental peace, which also has it’s own worth. I pay about €1,1k monthly which is a third of my take home pay, it’s still a steal when compared to other “Free Sector” houses in the Netherlands. Now.. I think I need to make some time to pick up the chicks… if I remember how… 😉