“What should I do with a cash lump sum?”

For most people, this could be an inheritance, bonus or other windfall.

But recently I had the fun challenge of discussing this with an owner whose business had just been through a partial sale to private equity. So they were sitting on a cash pile larger than most of us will ever handle. There are worse problems to have.

For the rest of us though, here are some thoughts on investing a lump sum…

The receipt of a large amount of cash can be an emotional rollercoaster.

If it’s an inheritance for example, the money is probably mixed up with a lot of emotions. If you have sold a business, you’ve likely been through a fraught period of months or even years.

So step one is to pause and sleep on it for a while and do nothing for a few weeks.

For most big life decisions, it’s good to avoid rushing to conclusions or acting in haste. So take some time before making decisions.

But, if several weeks later you still haven’t put the money to work, the greater risk is procrastination.

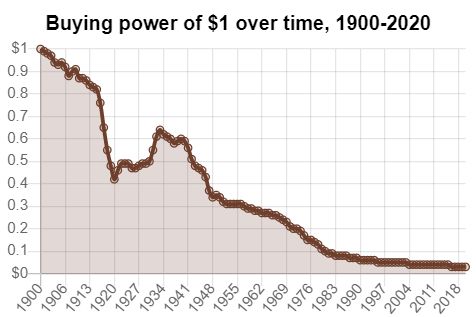

Inflation and money-printing never stop. They remorselessly erode the value of cash.

So this means that your cash is a bit like a beautiful ice sculpture at a party. You can’t see it melting away…but you know that it is disappearing before your eyes.

Hopefully you’ve already cleared all credit cards, overdrafts and lease finance payments some time ago but, if not, that should be the first use of the money.

Then there is the decision between mortgage paydown versus investing. Paying down the mortgage offers you a guaranteed rate of return equal to your mortgage interest rate…so let’s say ~4% currently.

That compares with total returns (dividends plus capital gains) of more like ~10% per year that have historically been achieved through investing in global equities.

So we are comparing a 4% “guaranteed” return from mortgage paydown versus a 10% prospective return from equities that is very much not guaranteed.

Let’s assume you’ve considered that and want to invest the money.

Is it better to invest a big lump sum of money all at once, or to drip-feed your cash into the market over time (known as $/£ cost averaging)?

This is one of those decisions where there are 2 aspects to the answer:

- The financial decision (expected returns)

- The emotional decision (your tolerance for risk or volatility)

All at once versus drip-feeding

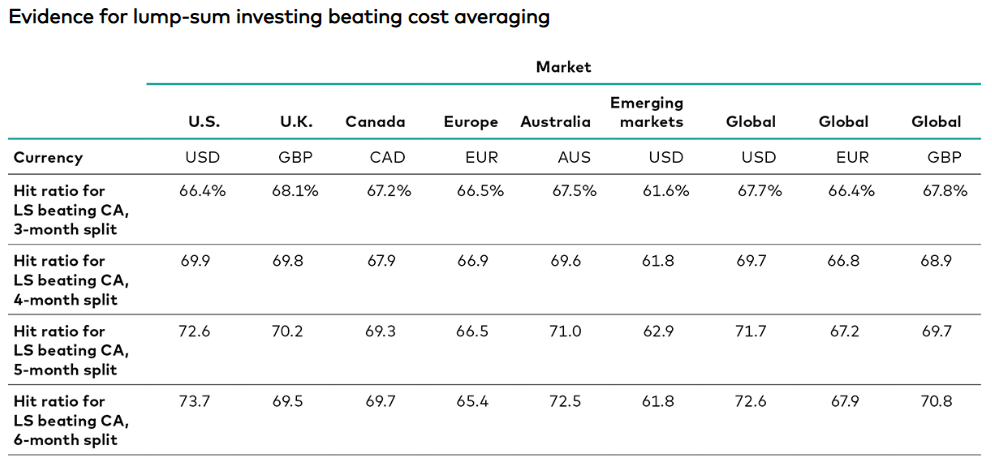

The empirical answer is clear and borne out in repeated studies: lump-sum investment beats cost-averaging approaches more than two-thirds of the time. Because equities outperform cash most of the time, getting your money to work faster has usually beaten scaling in.

Delaying has an opportunity cost. The months spent partly in cash represent lost expected returns. These higher equity returns represent the risk premium over cash returns required by other investors to compensate for volatility.

Dollar Cost Averaging can be a useful behavioural tool for getting comfortable with scaling into a desired end position. Cost averaging will by definition tend to smooth out the peaks and troughs of investment markets, but the data suggests that the best prospective returns come from lump-sum investing.

Let’s take a look at some evidence from Vanguard Research. Having compared the performance of cost averaging (CA) and lump-sum (LS) investing across various markets over rolling one-year periods between 1976 and 2022, Vanguard Research found that a lump-sum approach won between 61.6% and 73.7% of the time.

Vanguard looked at 3m, 4m, 5m and 6m periods for cost averaging. The relationship was clear: the longer the time it took to fully invest the capital, the worse that cost-averaging performed relative to lump-sum investing.

Notes: Hit ratio is defined as the outperformance of one strategy against the other after a one-year investment period. One-year rolling investment performance compares LS against CA. Our base case for CA is the three-month split, meaning splitting the investment into three equal parts and investing each one month apart. Source : Vanguard

So the empirical answer on whether to invest in one lump sum or via dripfeeding is clear.

If you are an investing ninja or an AI bot (without human emotions) you will be persuaded by the data. The data shows that because global equities have outperformed cash over the long term, getting fully invested earlier has historically worked out better in most cases. The sooner you get out of cash and into equities, the sooner the likely outperformance will start.

But if there is any risk that you are traumatised by a say 30% fall in the stockmarket that happened just after you invested, then you may be persuaded by the regret minimisation and the emotional advantage of dripfeeding.

In October 1987, the US stockmarket fell by ~30% in a week. It would have felt traumatic to anyone that had just invested a life-changing amount of money as a lump sum. Some would have been put off investing for life.

What fewer people remember is that it had fully recovered by Christmas the same year. Drip feeding through this period would have eased the pain.

Drip-feeding (aka pound-cost averaging) is useful as a way of managing our emotions, not because it’s likely to boost returns (it isn’t). According to Vanguard’s research (replicated in multiple studies), the lump sum approach wins two times out of three.

But the differences were marginal. Vanguard found that in the United States, lump sum investing led to an average ending value of 2.3% more than dollar cost averaging. The results were similar in the United Kingdom and Australia.

In other words, the gains from investing cash all at once are small on average. Personally, I’d choose the technique that I could execute whilst sleeping at night. There is value in regret-minimisation. The main thing is to stay in the game.

Investing a Lump Sum in 3 Steps

Step 1 : Start with your current asset allocation

We can only ever start from where we are. So that means looking at your current position. That means your current mix of assets.

Your current asset allocation is the mix of different assets that you own, analysed by asset class.

It’s really important to be able to summarise this in a spreadsheet. And, even better, to visualise it as a pie chart.

[Note: There are templates and worked examples for this in The Manual]

The gap between your current asset allocation and your target asset allocation will tell you where and how to invest the surplus cash.

Step 2: Do you have a target asset allocation?

A target asset allocation (your target mix of assets) acts as your “North Star” to keep your portfolio decisions taking you in the right direction.

A target asset allocation can be made complex but that is generally unnecessary.

Perhaps the best known target asset allocation is the classic institutional benchmark of 60% Equities : 40% Bonds…which limps on as a default in the minds of many investors, even though ever since 2008 government budget deficits and money-printing have doomed bonds to under-performance.

Sometimes less is more. For example, the simplest target asset allocation would be something like:

- A 6 month cash emergency fund;

- A paid off house; and

- Everything else in a global equities tracker fund

I am not saying that this is “right” or “wrong”. It’s just a very simple example of an asset allocation model.

If that were your mental model for asset allocation, it has some clear implications. You could start from the top and work down. First filling the emergency fund, then clearing the mortgage and then investing whatever remained in the stockmarket.

You can add in other asset classes as diversifiers. Gold, crypto and commodities are all volatile. But at least they are volatile in ways that tend to offset each other (and offset the volatility of equities).

Here is a neat example… earlier this year, gold and oil acted as almost perfect diversifiers for each other:

By adding either negatively correlated or imperfectly correlated assets, equity volatility is mitigated. The challenge is asset class correlations are constantly shifting over time.

Here’s my point. Having a target asset allocation helps guide the decision of what to do with any surplus cash, whether from windfall, inheritance or bonus.

Having a target asset allocation is necessary for rebalancing each year, which tends to encourage buying low and selling high.

If you don’t yet have a target asset allocation, well there is some homework for you!

[Note: There are templates and worked examples for this on The Manual]

Step 3 : The difference between the current and the target asset allocation provides the roadmap

Once you have a target asset allocation, you create a gap analysis versus your current asset allocation. This shows you where the new cash needs to go.

You choose your time horizon for getting fully invested and you use tax shelters (e.g. ISAs and pensions) as much as you can.

It’s then just a matter of ensuring that you have an appropriate choice of funds to choose to implement the asset allocation.

The simplest way to get global equity exposure is via a tracker fund: either a traditional open ended mutual fund OR an exchange traded fund (ETF).

ETFs tend to have the lowest fees and there are plenty of choices; here are just a few examples of global equity ETFs:

- Vanguard All World ETF (Ticker: VWRP) – Fees 0.19%

- Vanguard Developed World ETF (Ticker: VHVG) – Fees 0.12%

- Invesco FTSE All World (Ticker: FWRA) – Fees 0.15%

- SPDR MSCI All Country World ETF (Ticker: SWLD) – Fees 0.12%

As ever, the main thing is not to get stuck.

Happy investing!

Barney

If you’d like to discuss financial coaching or career coaching, please set up an introductory call with me here.

A subscription to The Manual gives you access to target asset allocation models, templates and example spreadsheets