It’s been a while since I did a “back to basics” post about investing. So here’s a quick reminder…

The stockmarket is the best game in town for long-term wealth building.

Long term returns on global equities have been about ~10% per year globally. As of May 2026, the MSCI World equity index has returned 9.9% per year since 1988.

At 10% per year, your portfolio doubles every ~7 years. There are no guarantees but your best shot over the long term is to chuck as much money as you can into your compounding machine.

You are going to want to go as high in terms of % asset allocation to equities as possible given your ability to bear risk.

Inflation is the enemy. Companies can react to inflationary pressures (e.g. from higher oil prices) by raising prices, profits and dividends.

In contrast, as government debt and the money supply expands (and ever more money gets printed), bonds and cash are doomed to lose their real value (purchasing power). So equities win over the long term.

In order to buy into the stockmarket as simply as possible you need to choose 2 things:

- an online broker / investment platform;

- a global equities fund.

Choose a platform

First up: choose an online broker (also known as an investment platform) and open an account.

Because all brokers / platforms in the UK are regulated by the Financial Conduct Authority, they all meet a certain standards for financial strength and the legal separation of client assets protects you even if in the unlikely event that they go bust.

You can compare the fees of different online brokers / platforms using this handy Monevator guide.

Choose a fund

Now we need to choose a fund. What’s a fund? I think of a fund as a box that contains share certificates…pieces of paper (now electronic) that denote part-ownership of companies.

A global tracker fund is a pooled investment vehicle that owns a little slice of all the biggest companies of the world. The value of the “box” is determined by the value of all the shares that it owns.

When you invest in a global equities fund, you benefit from broad diversification in a one stop shop. You don’t have to worry how individual companies are doing because, if one company is losing, others will be winning. Once you own a global index tracker, the system is working for you.

We are looking for funds that actually own the underlying shares (i.e. physical replication) rather than synthetic exposure via a derivative arrangement with an investment bank.

In Exchange-Traded Funds (ETFs), optimised exposure (or “sampling”) refers to a physical replication method where a fund buys a representative selection of securities from its underlying benchmark index, rather than holding every single asset

But what to buy? With thousands of heavily marketed funds, it’s easy to get bombarded and over-loaded with information.

The simplest way to get global equity exposure is via a tracker fund: either a traditional open ended mutual fund or an exchange traded fund (ETF).

As I may have mentioned before, just investing in a global equities tracker fund is a pretty tough strategy to beat. Its simple, its low cost, it gives global diversification in a one stop shop.

We like Vanguard because it’s owned by its customers, but it’s not the only game in town. And these days, it’s not necessarily the cheapest either.

Looking at Vanguard’s UK & European product range, there are plenty of options when it comes to global tracker funds. I have picked the following three for your further research:

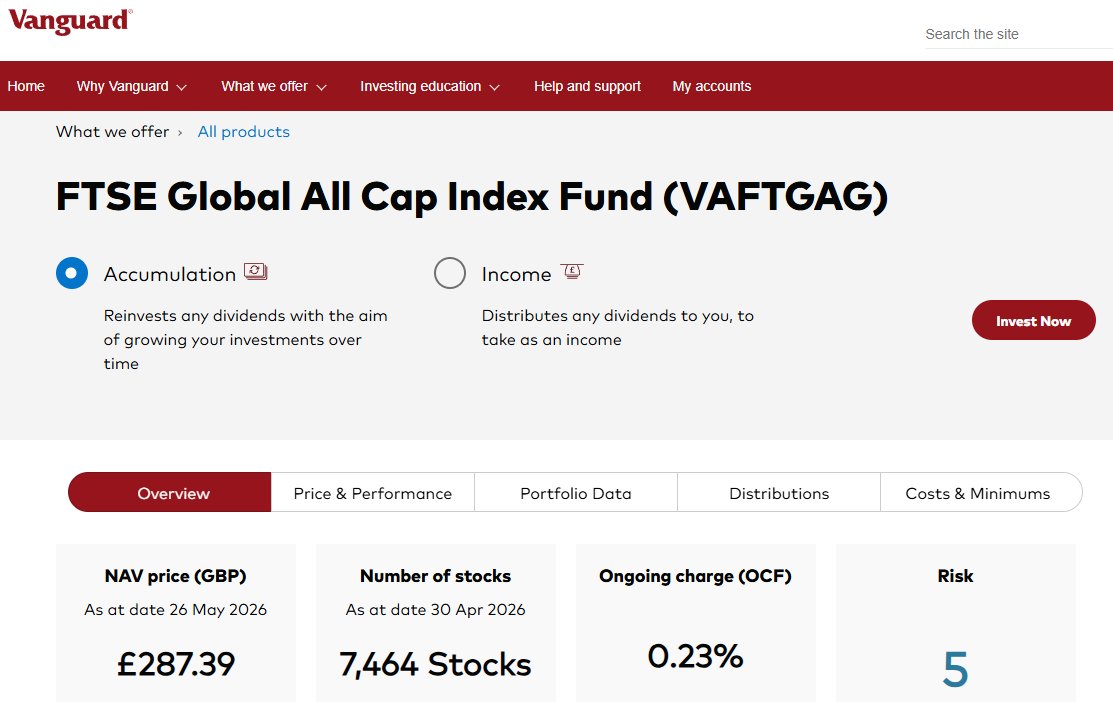

- The Vanguard FTSE Global All Cap Index Fund

- The Vanguard FTSE All World ETF

- The Vanguard FTSE Developed World ETF

The Vanguard FTSE Global All Cap Index Fund

The Vanguard FTSE Global All Cap Index Fund includes smaller companies as well as global giants.

The number of companies held by the fund is a whopping ~7,500. So we get the broadest diversification at low cost. What’s not to like?

This is structured as an open ended mutual fund so you know that you are buying in at the net asset value. There is no intra-day trading but that’s a positive. It’s suitable for all investment sizes, even very large lump sums as there is no risk of market disturbance or slippage.

ETFs and mutual funds are available either in dividend paying form (income units which pay cash dividends) or in automatic reinvestment form (accumulation units which use the cash dividends to buy you a greater share of the fund).

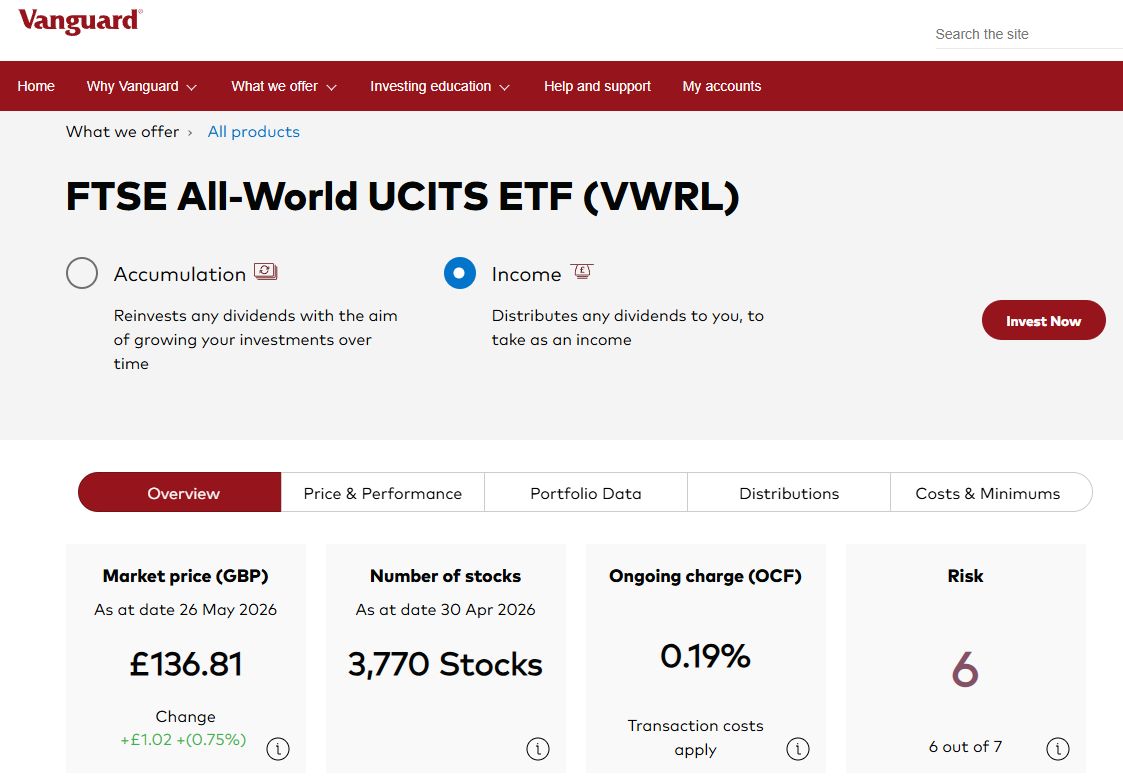

The Vanguard FTSE All-World UCITS ETF

This does the job of one stop shop with low fees (TER of 0.19%). It owns ~3,800 of the biggest companies in the world from all countries.

It’s structured as an exchange traded fund (ETF) as are the rest of the trackers on the list. That’s mainly because ETFs tend to have lower fees than the equivalent unquoted mutual funds.

Vanguard’s product range includes both exchange traded funds and traditional open ended mutual funds. What’s the difference? Well, in summary, exchange traded funds trade on stock exchanges during market hours.

For the user, an ETF is much quicker to get your order filled and you know the price at the moment you buy. For the battle-hardened investor turned bargain hunter, this makes ETFs ideal when buying in the middle of a market crash.

In contrast, with traditional funds you have to wait a few days for the transaction to get processed at the prevailing net asset value.

The bottom line is that a Vanguard exchange traded fund and a Vanguard traditional mutual fund are far more similar than they are different. Both do the job nicely.

Don’t be put off by the fact that the title of the fund says USD (it’s reporting currency is US dollars). It’s traded on the London Stock Exchange and priced and traded in GBP.

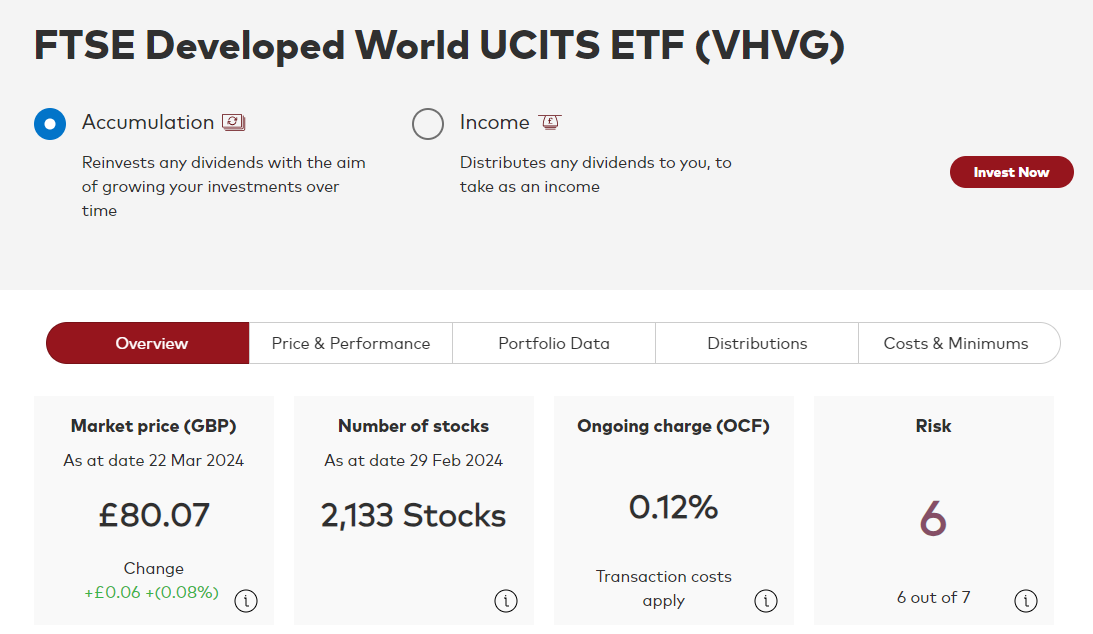

The Vanguard FTSE Developed World UCITS ETF

This exchange traded fund excludes emerging markets.

Why would you do that? Well it’s cheaper for one thing, with annual fees of only 0.12% which makes it the lowest cost fund of the bunch.

But another good reason perhaps would be if you don’t want exposure to emerging markets due to their political risk, governance standards or any ethical concerns. Or maybe you already have enough emerging markets exposure via a specialist fund?

Again, don’t be put off by the fact that the title of the fund says USD (it’s reporting currency is US dollars). It’s traded on the London Stock Exchange and priced and traded in GBP.

Just to show that I am not biased in favour of Vanguard, here are 3 examples of global equity ETFs from other fund providers:

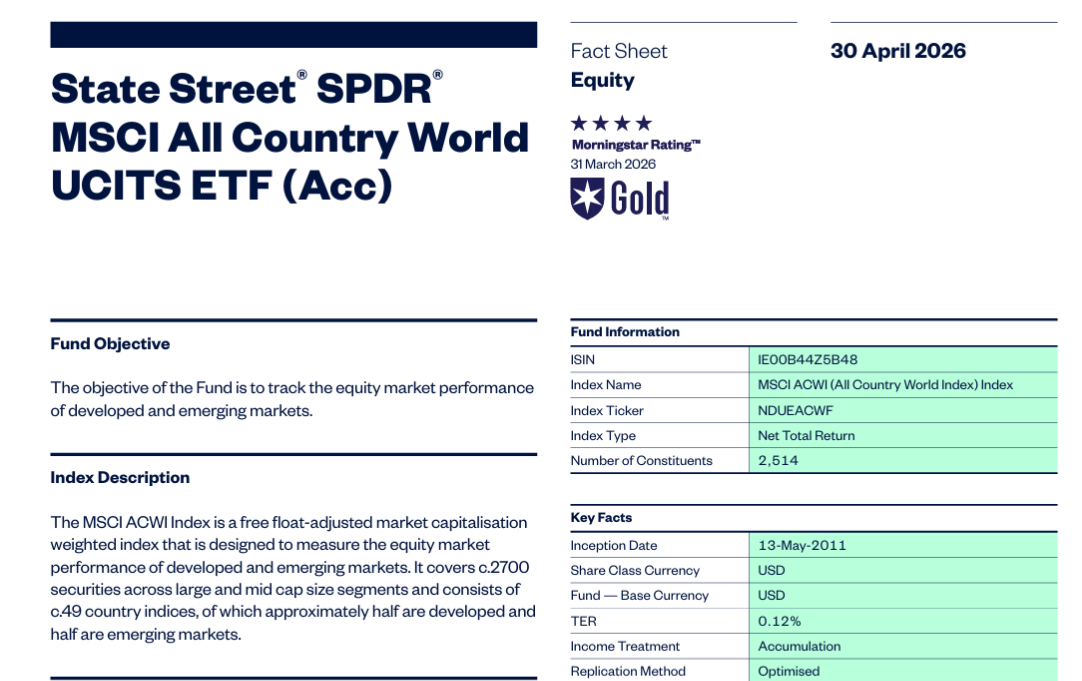

SPDR MSCI All Country World UCITS ETF – Fees 0.12%

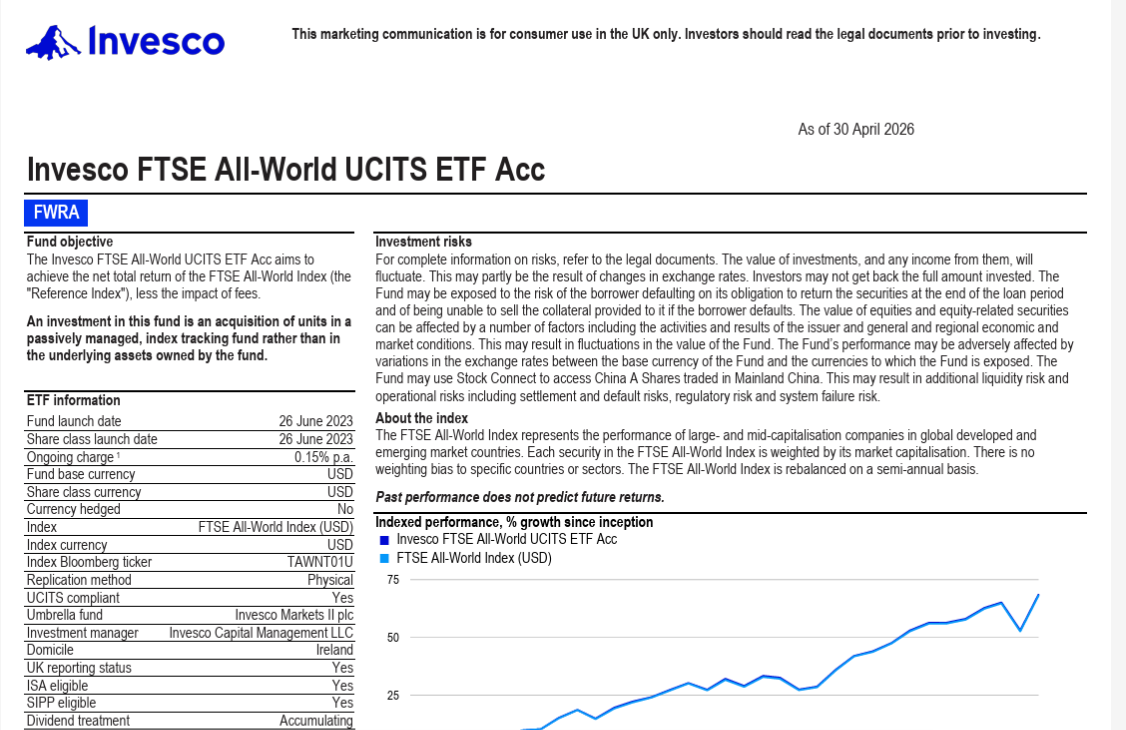

Invesco FTSE All-World UCITS ETF – Fees 0.15%

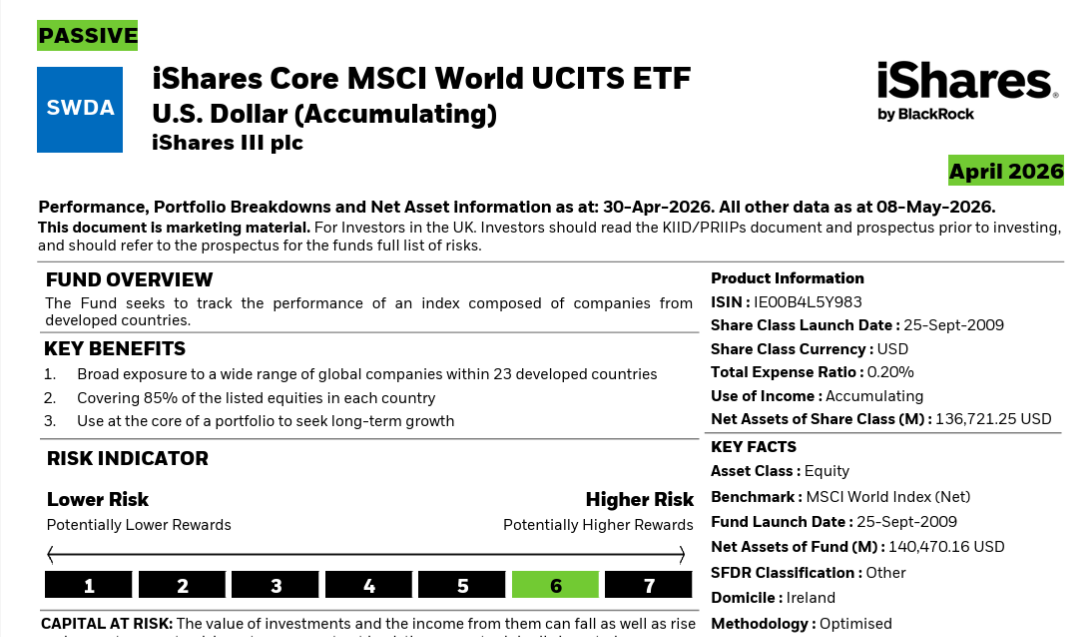

iShares Core MSCI World UCITS ETF – Fees 0.20%

There are many other ETFs and open ended funds out there but these form an excellent starting line-up for you to look at.

People will tell you its more complicated than this. And you could make things more complicated…but would it justify the extra time, cost and effort involved?

All you have to do now is make a choice and remember to never sell in panic during a crash.

Happy investing!

Barney

Please hit reply if you’d like to talk about financial coaching or career coaching.